Adapting to EIS Invoicing and Tax Filing with BIR CAS-Ready NetSuite ERP

The Philippine tax landscape is undergoing one of its biggest digital transformations in decades. Through Revenue Regulations (RR) No. 11-2025, the Bureau of Internal Revenue (BIR) has formally introduced the Electronic Invoicing / Electronic Sales Reporting System (EIS), a nationwide initiative that will fundamentally change how businesses issue invoices and report sales data.

This reform is aligned with the CREATE MORE Act (Republic Act No. 12066) and builds upon earlier digitalization efforts introduced under the TRAIN Law of 2018. The goal is to modernize tax administration, increase transparency, and allow the BIR to monitor sales transactions more efficiently.

Under the new mandate, selected taxpayers must issue invoices in a structured digital format and transmit transaction data electronically to the BIR through the Electronic Invoicing System (EIS).

This means businesses can no longer rely solely on traditional paper invoices or loosely formatted digital documents. Instead, invoices must be generated through BIR-registered systems capable of producing structured data, such as a Computerized Accounting System (CAS) compliant ERP platform.

For companies using enterprise systems, this transition can be significantly smoother because modern ERPs already support automated invoice generation, structured financial records, and real-time reporting.

Ultimately, the e-invoicing mandate aims to:

- Improve tax transparency

- Reduce tax evasion and invoice manipulation

- Streamline accounting and reporting processes

- Enable faster audits and data validation

While the regulation introduces new responsibilities for businesses it also presents an opportunity for companies, especially SMEs, to modernize their accounting systems and improve operations.

What does E-Invoicing mean?

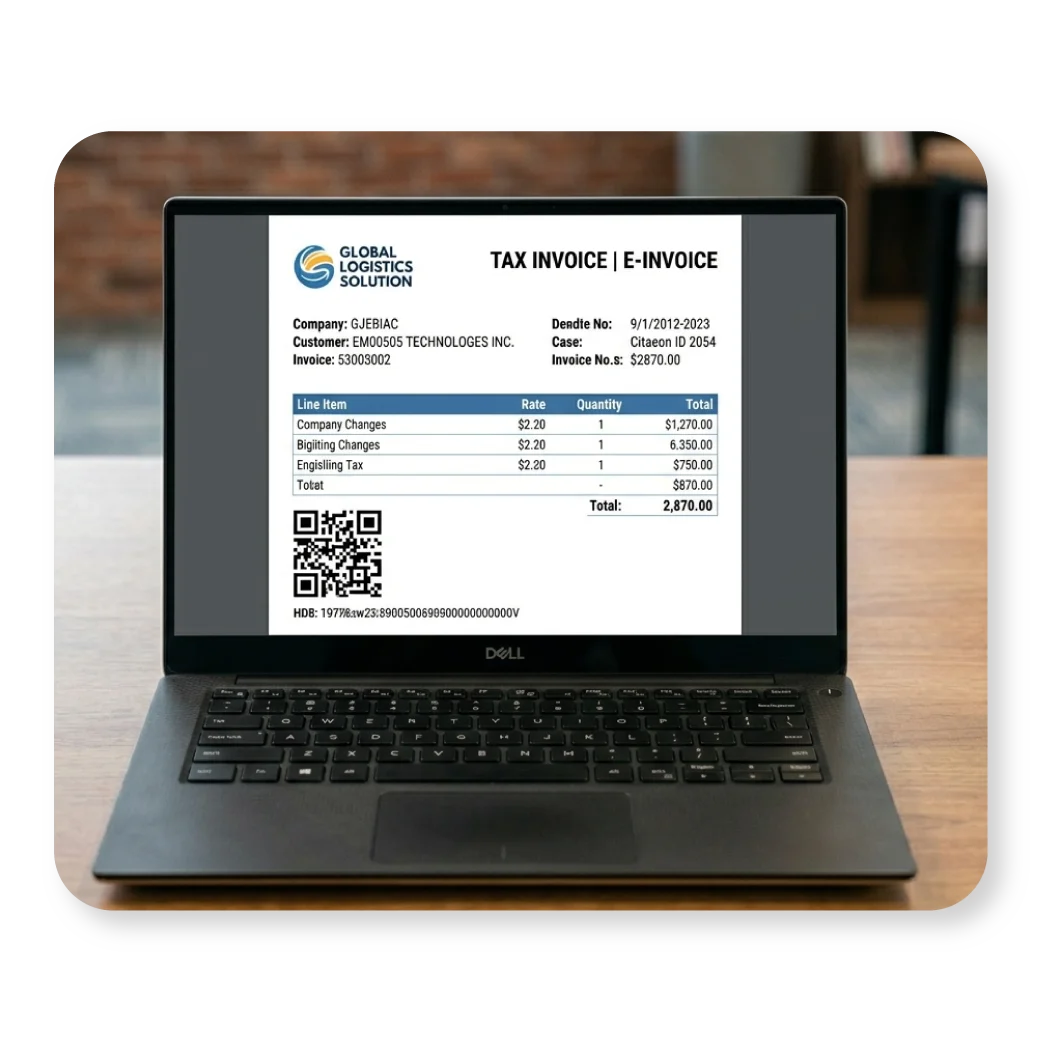

At its core, e-invoicing refers to issuing invoices electronically in a structured data format rather than relying on paper receipts or unstructured digital files.

This structured format allows the invoice data to be automatically processed by both the company’s accounting system and the BIR’s reporting platform.

Unlike traditional invoices, structured e-invoices contain machine-readable fields that make it easier to validate transactions and calculate taxes.

For example, a structured e-invoice typically includes:

- Invoice number

- Transaction date

- Supplier and customer information

- Description of goods or services

- Itemized pricing details

- VAT calculations and tax treatment

Technical Requirements for EIS Reporting in the Philippines

To ensure consistency and accuracy, the BIR has established specific technical standards for electronic invoices.

System Integration

Before using any ERP system, businesses must ensure that their system:

- Underwent EIS certification and

- Obtained a Permit to Transmit (PTT)

So they can properly send data to the BIR.

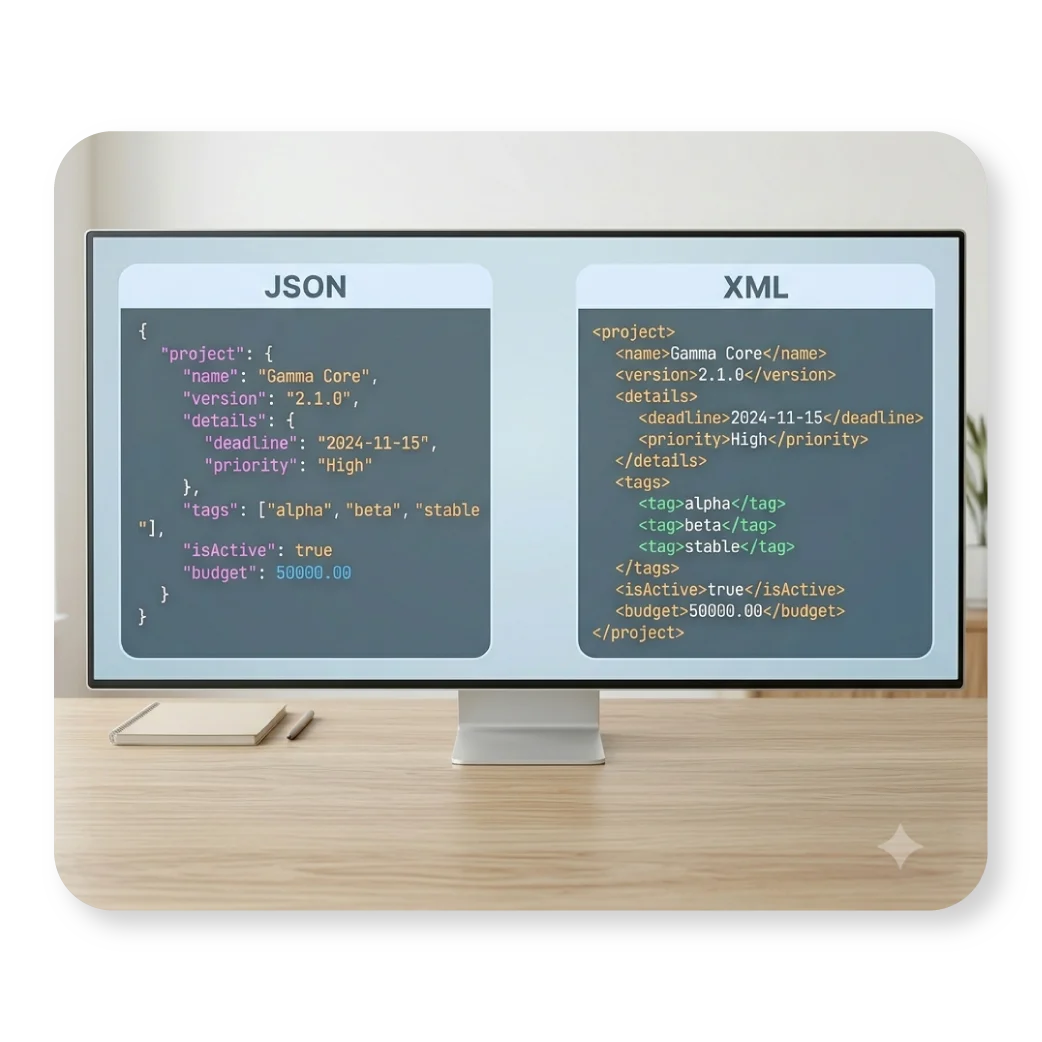

Structured Data Format

Invoices from these systems must be generated in a structured digital format that follows the BIR’s schema. Common formats include:

- JSON

- XML

Structured formats allow systems to extract key data fields automatically and transmit them to the BIR. Because the data is machine-readable, it can be transmitted electronically to the BIR’s reporting system for validation and record-keeping.

This requirement reinforces the importance of ERP platforms like BIR CAS-Ready NetSuite, which integrates accounting, invoicing, and tax reporting processes and can generate these structured invoices directly from their accounting platform.

Sales Data Transmission

Invoice data must be transmitted to the BIR through a secure API or system-to-system interface.

The reporting window is generally:

- Real-time or near-real-time, or

- Within three calendar days of the transaction

Failure to transmit invoice data within this timeframe may result in compliance issues.

This requirement significantly changes traditional workflows. Instead of preparing reports at the end of the month or quarter, businesses must ensure their systems capture and report transaction data almost immediately.

For SMEs still relying on spreadsheets or manual invoice processes, this requirement can be particularly challenging.

Electronic Archiving

Businesses must maintain a digital archive of their invoices and transmission records.

These records must be:

- Secure

- Tamper-proof

- Accessible for BIR audits

Philippine tax law requires businesses to retain accounting records for at least 10 years.

This includes:

- The original structured invoice data (JSON/XML)

- Human-readable versions (PDF or print)

- Transmission confirmations

- Audit logs and metadata

Proper archiving ensures companies can retrieve invoice records quickly when needed.

Error Corrections and Adjustments

Mistakes in invoices must be corrected carefully to maintain an accurate audit trail. Businesses cannot simply edit an existing invoice. Instead, corrections must follow formal processes.

Cancellation and Reissuance

If an invoice contains a major error, it must be cancelled and replaced with a new invoice referencing the original.

Credit and Debit Notes

For adjustments after the invoice has been issued—such as price changes or refunds—businesses must issue credit or debit notes.

These documents must also be transmitted to the BIR through the EIS.

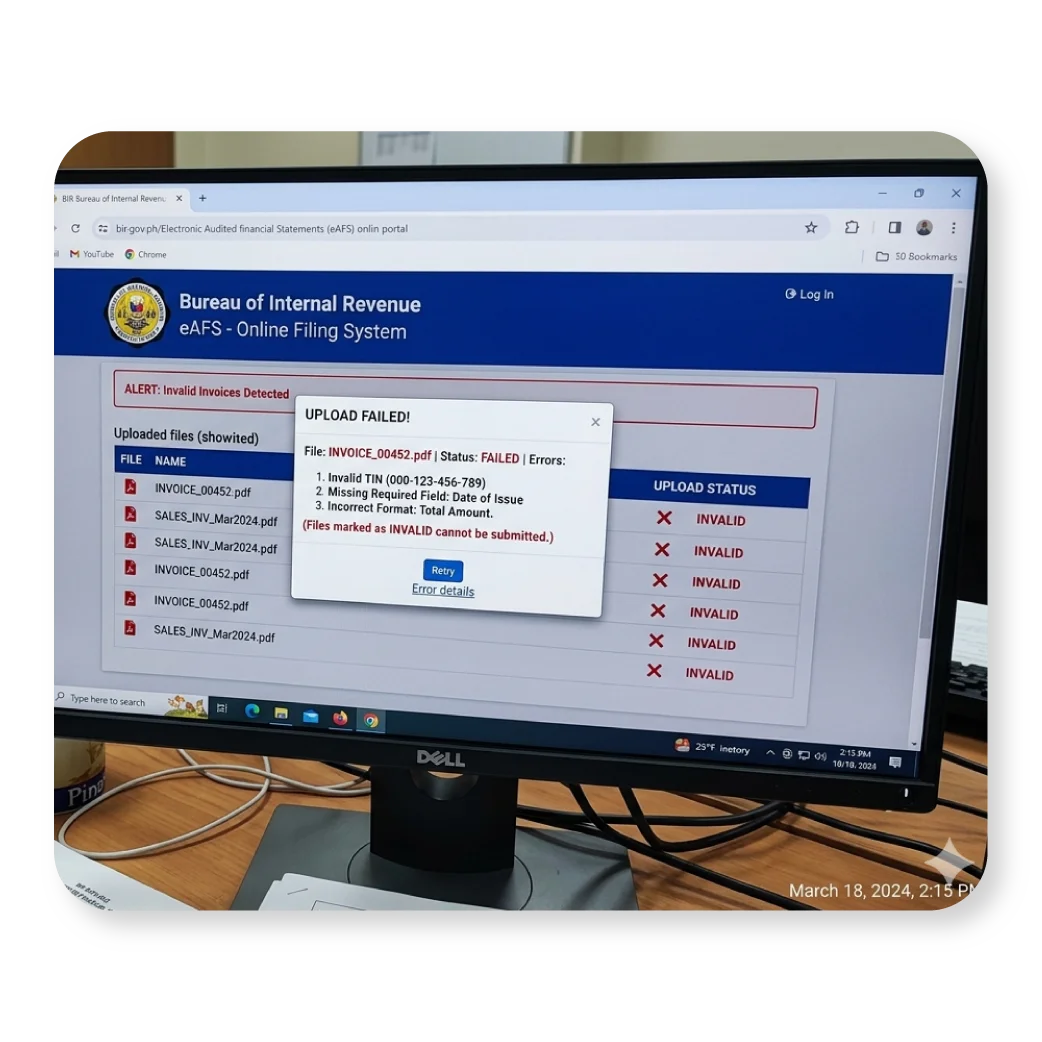

What does NOT qualify as an E-Invoice?

One common misconception is that simply digitizing an invoice qualifies as e-invoicing.

However, under the regulation:

- Scanned copies of paper invoices

- Photographs of printed receipts

- PDFs without structured data

do not qualify as electronic invoices.

Only invoices generated by a system capable of structured data output and electronic transmission will be recognized as compliant.

This requirement is one reason many organizations are adopting NetSuite ERP, which can generate structured financial data directly from sales and accounting transactions.

E-Invoicing Implementation Timeline

The rollout of electronic invoicing in the Philippines has been gradual, with several milestones along the way. This is to give businesses enough time to prepare their systems and processes.

2018 – TRAIN Law

The legal basis for electronic invoicing is established.

2022 – Initial Framework

Revenue Regulations RR 8-2022 defined the structure and reporting requirements.

July 2022 – Pilot Program

A pilot program began with 100 large taxpayers.

2022–2023 – Pilot Challenges

Technical challenges temporarily paused the rollout.

February 2025 – Expansion Resumes

Revenue Regulations RR 11-2025 restarted the rollout and provided businesses time to prepare.

February 27, 2025

The BIR issued Revenue Regulations No. 11-2025, establishing the structured e-invoicing framework.

March 14, 2025

The regulation officially took effect.

September 2025 – Deadline Extension

RR 26-2025 extended the compliance deadline.

March 14, 2026

The original deadline for covered taxpayers to begin issuing structured electronic invoices.

December 31, 2026

The BIR extended the compliance deadline for certain taxpayers under RR 26-2025.

January 1, 2027 – Mandatory Implementation

Phase 1 taxpayers must begin issuing electronic invoices and reporting through EIS.

Future phases will expand coverage to additional taxpayers.

This phased approach allows businesses to gradually adapt their accounting systems and reporting workflows. However, the timeline also signals that digital invoicing will soon become the standard across the Philippine business landscape.

Companies that begin upgrading their systems early, particularly those implementing NetSuite EIS reporting will likely experience fewer disruptions when enforcement begins.

Businesses Required to Comply with E-Invoicing

Not all businesses must adopt e-invoicing immediately. The BIR is prioritizing taxpayers that already operate with advanced systems or high transaction volumes.

Taxpayers Currently Covered

Under RR 11-2025, the mandate applies to:

1. E-Commerce Businesses

Companies engaged in digital or online transactions, including:

- Online retailers

- Digital service providers

- Marketplace operators

- Social commerce businesses

Because these businesses already rely heavily on digital systems with a large volume of digital transactions, integrating e-invoicing is often easier.

2. Large Taxpayers

Businesses under the BIR’s Large Taxpayers Service (LTS) are also included in the initial rollout as they typically have significant annual revenue. Under RA 11976, businesses generating over ₱1 billion in annual gross sales may be classified as large taxpayers.

3. Businesses Using Computerized Accounting Systems

Companies already using:

- Computerized Accounting Systems (CAS)

- Computerized Books of Accounts (CBA)

- Electronic invoicing systems

Transactions Currently Covered

The mandate also applies to a wide range of transactions conducted by businesses operating in the Philippines.

1. Domestic Transactions

Electronic invoicing applies to:

- Business-to-Business (B2B) sales

- Business-to-Consumer (B2C) transactions

- Business-to-Government (B2G) sales

For example:

- A wholesaler selling products to a retail store

- A restaurant issuing receipts to customers

- A supplier invoicing a government agency

As long as the transaction value meets the ₱100 minimum threshold, it must be included in electronic reporting.

2. Export Transactions

Exports will also be included in the reporting framework. Even though export sales are typically zero-rated for VAT, businesses must still generate electronic invoices reflecting the correct tax treatment.

3. Imports and Cross-Border Purchases

Imports are handled through a separate system called Customs Electronic Invoicing (CEI).

Under this framework, foreign exporters issuing invoices for goods entering the Philippines will eventually need to provide structured digital invoices. However, foreign companies are generally not required to follow the domestic e-invoicing rules unless they are VAT-registered in the Philippines.

4. Other Transactions

The system also applies to:

- VAT-exempt sales

- Zero-rated transactions

- Special tax scenarios

Additional Businesses That May Be Included Later

As the system evolves, additional taxpayer groups will be required to adopt e-invoicing.

These may include:

- Exporters of goods and services

- Registered Business Enterprises (RBEs) enjoying tax incentives

- Businesses using Point-of-Sale (POS) systems

- Other taxpayers identified by the BIR Commissioner

If a company operates with multiple branches, both the head office and branch locations must comply.

Micro-Enterprise Exemption

Micro enterprises—generally those with annual sales below ₱3 million—are currently exempt from the mandatory requirement.

However, they may still choose to adopt electronic invoicing voluntarily. This voluntary adoption can help smaller businesses modernize their accounting processes and prepare for future compliance requirements.

What this means for SMEs

While large companies are the first to be affected, SMEs should not assume they are exempt forever.

Eventually, most VAT-registered businesses will need to comply.

This means SMEs must begin preparing by:

- Modernizing their accounting systems

- Implementing electronic invoicing capabilities

- Automating tax reporting processes

Although the transition may require initial investment, it also offers long-term benefits:

Increased Efficiency. Electronic invoicing automates many tasks traditionally handled by accounting teams. Invoices can be generated, validated, and transmitted automatically, reducing manual work.

Improved Accuracy. Structured data reduces human errors in tax calculations and financial reporting. This improves overall compliance with BIR requirements.

Faster Audits and Reconciliation. Because the BIR can access transaction data electronically, audits may become faster and more efficient. Businesses also benefit from quicker reconciliation of sales and financial records.

Lower Administrative Costs. Digital invoicing eliminates many expenses associated with:

- Printing invoices

- Storing physical records

- Manual reconciliation

Fraud Prevention. Electronic records make it harder to manipulate invoices or conceal transactions, reducing tax fraud.

For many organizations, upgrading their ERP to support tax filing automation is a practical way to meet these requirements. They are also often better positioned to handle these changes because their accounting, sales, and reporting processes are already integrated.

Why ERP Systems Like NetSuite Are Becoming Essential

As e-invoicing and digital tax reporting become standard, many businesses are realizing that traditional accounting tools may no longer be sufficient.

ERP platforms provide a more scalable solution.

With NetSuite ERP, companies can integrate:

- Accounting

- Sales transactions

- Invoicing

- Tax calculations

- Compliance reporting

This ERP solution also enables businesses to support BIR CAS compliance, automate tax filing, and meet the requirements of EIS reporting in the Philippines.

For growing SMEs in the Philippines, adopting an ERP system can help build a more efficient and scalable business infrastructure.

Risks of Non-Compliance

Businesses that fail to adopt the required electronic invoicing system may face several risks.

Invalid Invoices. Invoices issued outside the structured format may not be recognized as valid electronic invoices under BIR regulations.

Penalties and Sanctions. Companies that fail to comply may face financial penalties or disallowed tax deductions.

These include:

1. Failure to Issue Proper Invoices

- Fines ranging from ₱1,000 to ₱50,000 per offense

- Possible imprisonment of 2 to 4 years

2. Failure to Transmit Invoice Data

- A daily penalty of ₱10,000 or 0.1% of annual net income, whichever is higher

If violations exceed 180 days in a year, the BIR may order business closure.

3. False or Incorrect Reporting

Penalties may include fines up to ₱10 million and possible imprisonment.

Increased Audit Risk. Non-standard invoices may attract additional scrutiny during tax audits.

Operational Disruptions. Businesses that delay system upgrades may struggle to adapt quickly once enforcement begins.

Tax Incentives for Adopting E-Invoicing

To encourage adoption, the Philippine government is offering tax incentives for businesses that implement electronic invoicing systems.

Under the CREATE MORE Act, companies can claim additional deductions for system implementation costs.

These incentives include:

- 100% deduction for micro and small enterprises

- 50% deduction for medium and large businesses

This incentive helps offset the cost of upgrading accounting systems or implementing ERP solutions.

Preparing Your Business for E-Invoicing

To avoid disruptions, businesses should begin preparing for electronic invoicing well before the compliance deadline.

Key preparation steps include:

- Evaluating Existing Systems

Companies should review whether their accounting or ERP systems can generate structured invoices and support electronic reporting. - Integrate and Test Systems

System integration typically involves connecting the company’s invoicing system with the BIR reporting platform through APIs.

Testing ensures that invoice data is transmitted correctly. - Train Staff

Finance and accounting teams must understand how to generate structured invoices, transmit data, and maintain digital records.

Working with Experts for ERP Implementation

Successfully implementing NetSuite ERP requires careful system configuration, integration, and compliance planning.

Mustard Seed Systems Corporation is an established ERP solutions provider in the Philippines with expertise in implementing Oracle NetSuite ERP for organizations across multiple industries.

As a NetSuite implementation partner, the company helps businesses configure ERP systems to support:

- BIR CAS compliance requirements

- Structured invoice generation

- NetSuite EIS reporting and integrations

- NetSuite tax filing automation

Working with experienced implementation specialists ensures that NetSuite is properly configured to align with Philippine regulatory standards while supporting long-term financial management and reporting.

For SMEs and growing enterprises, having a local implementation partner can be particularly valuable. Providers familiar with Philippine regulations understand how to configure ERP systems to support:

- CAS registration and reporting requirements

- Structured electronic invoicing formats

- Financial reporting aligned with BIR standards

- Automated tax calculations and reconciliation

With proper implementation, businesses can fully leverage NetSuite and ensure that accounting data, invoices, and tax reports remain consistent.